Probability parser¶

bayesloop as a probabilistic programming framework is focused on

two-level hierarchical models for time series analysis, and is therefore

not as flexible as other frameworks.

PyMC3, for example, allows the

user to create hierarchical models of any structure and to apply

arbitrary arithmetic operations on the random variables contained in the

model. While bayesloop allows the user to build custom low-level

(observation) models and choose from a variety of high-level

(transition) models, one has no direct influence on the choice of

parameters. In other words, the Gaussian observation model includes

the parameters mean and standard deviation, but there is no direct

way of evaluating the variance or the ratio of mean and standard

deviation instead. In many applications, however, these combinations or

transformed variables are the key to informed desicions! In finance, for

example, the performance of a financial asset is often evaluated by its

Sharpe ratio \(S\):

where \(\mu\) is the expected return of the financial asset,

\(\mu_0\) is the risk-free return, and \(\sigma\) is the

volatility. Assuming Gaussian returns, we can obtain time-varying

estimates of \(\mu\) and \(\sigma\) with a simple Gaussian

observation model with bayesloop, while \(\mu_0\) is just a

series of given numbers we may obtain from the central bank.

This tutorial shows how to evaluate arithmetic combinations of inferred

parameter distributions after the model has been fitted, using the

eval method of the Study class and the Parser class. With

these tools, we compute the probability that the time-varying Sharpe

ratio of a simulated series of returns is greater than one (a common

threshold for investing in financial assets).

First, we simulate a fictious series of price fluctuations. Here we assume gradual changes in the expected return, the risk-free return and the volatility. Based on the expected return and the volatility, we sample the observed price fluctuations based on a Gaussian distribution:

In [1]:

%matplotlib inline

import matplotlib.pyplot as plt # plotting

import seaborn as sns # nicer plots

sns.set_style('whitegrid') # plot styling

sns.set_color_codes()

import bayesloop as bl

import numpy as np

mu_sim = np.concatenate([np.linspace(-0.1, 0.3, 250), np.linspace(0.3, 0.1, 250)])

sigma_sim = np.linspace(0.05, 0.2, 500)

mu0 = np.linspace(0.02, 0.01, 500)

sharpe_sim = (mu_sim-mu0)/sigma_sim

np.random.seed(123456)

data = mu_sim + sigma_sim*np.random.randn(500)

plt.figure(figsize=(10, 11))

plt.subplot2grid((7, 1), (0, 0))

plt.plot(mu_sim, c='b', lw=3, label='Expected return $\mathregular{\mu}$')

plt.xticks([100, 200, 300, 400], ['', '', '', ''])

plt.xlim([0, 500])

plt.legend(loc='upper left')

plt.subplot2grid((7, 1), (1, 0))

plt.plot(mu0, c='g', lw=3, label='Risk-free return $\mathregular{\mu_0}$')

plt.xticks([100, 200, 300, 400], ['', '', '', ''])

plt.xlim([0, 500])

plt.legend(loc='upper right')

plt.subplot2grid((7, 1), (2, 0))

plt.plot(sigma_sim, c='r', lw=3, label='Volatility $\mathregular{\sigma}$')

plt.xticks([100, 200, 300, 400], ['', '', '', ''])

plt.xlim([0, 500])

plt.legend(loc='upper left')

plt.subplot2grid((7, 1), (3, 0), rowspan=2)

plt.plot(sharpe_sim, lw=4, c='orange', label='Sharpe ratio S')

plt.xticks([100, 200, 300, 400], ['', '', '', ''])

plt.axhline(y=1, c='0.2', ls='dashed', lw=1, label='Investment threshold (S=1)')

plt.xlim([0, 500])

plt.legend(loc='lower right')

plt.subplot2grid((7, 1), (5, 0), rowspan=2)

plt.plot(data, c='0.2', lw=1.5, label='Simulated price fluctuations')

plt.xlim([0, 500])

plt.ylim([-0.65, 0.65])

plt.legend(loc='lower left')

plt.xlabel('Time [arbitrary units]');

To infer the time-varying expected return \(\mu\) and volatility

\(\sigma\) from the simulated price fluctuations, we assume a

Gaussian observation model. The two parameters of this observation

model are themselves subject to a GaussianRandomWalk, the transition

model of the study. For simplicity, we set fixed magnitudes for the

parameter fluctuations (sigma_mu, sigma_stdev):

In [2]:

S = bl.Study()

S.load(data)

L = bl.om.Gaussian('mu', bl.cint(-0.5, 0.5, 100), 'sigma', bl.oint(0, 0.5, 100))

T = bl.tm.CombinedTransitionModel(

bl.tm.GaussianRandomWalk('sigma_mu', 0.01, target='mu'),

bl.tm.GaussianRandomWalk('sigma_stdev', 0.005, target='sigma')

)

S.set(L, T)

S.fit()

+ Created new study.

+ Successfully imported array.

+ Observation model: Gaussian observations. Parameter(s): ['mu', 'sigma']

+ Transition model: Combined transition model. Hyper-Parameter(s): ['sigma_mu', 'sigma_stdev']

+ Started new fit:

+ Formatted data.

+ Set prior (function): jeffreys. Values have been re-normalized.

+ Finished forward pass.

+ Log10-evidence: 130.79643

+ Finished backward pass.

+ Computed mean parameter values.

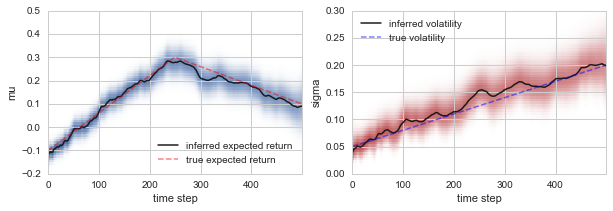

Plotting the inferred expected return and volatility against the true underlying values used in the simulation, we find that the time-varying parameter model we defined above nicely captures the variations in the performance of the fictious financial asset:

In [3]:

plt.figure(figsize=(10, 3))

plt.subplot2grid((1, 2), (0, 0))

S.plot('mu', color='b', label='inferred expected return')

plt.plot(mu_sim, lw=1.5, c='red', ls='dashed', alpha=0.5, label='true expected return')

plt.ylim([-0.2, 0.5])

plt.legend(loc='lower right')

plt.subplot2grid((1, 2), (0, 1))

S.plot('sigma', color='r', label='inferred volatility')

plt.plot(sigma_sim, lw=1.5, c='blue', ls='dashed', alpha=0.5, label='true volatility')

plt.ylim([0, 0.3])

plt.legend(loc='upper left');

Based on these inferred parameter distributions, we can now evaluate

probabilities in the form of inequalities using the eval function of

the Study class. For example, we can evaluate the probability of a

positive expected return at time step 50:

In [4]:

S.eval('mu > 0.', t=50);

P(mu > 0.) = 0.2486016146556542

By default, eval prints out the resulting probability. This behavior

can be controlled with the keyword-argument silent. eval further

returns the value, for further processing:

In [5]:

p = S.eval('mu > 0.', t=50, silent=True)

print(p)

0.248601614656

The keyword-argument t is not the only way to define the time step

at which to evaluate the probability value. One can also use the @

operator. In this example, we ask for the probability of a volatility

value smaller than 0.2 at t=400:

In [6]:

S.eval('sigma@400 < 0.2');

P(sigma@400 < 0.2) = 0.934624296075193

The evaluation of probability values is not restricted to a single time

step, one may also be interested whether the expected return at

t=100 is greater than at t=400. Note that bayesloop does not

infer the joint parameter distribution of all time steps, but the

conditional joint parameter distributions for each time step

iteratively. This means that correlations between the parameter at

different time steps are ignored by the eval method. Further note

that comparing parameters at different time steps may result in a fairly

long computation time and a lot of RAM usage, as bayesloop has to

take into account all possible combinations of parameter values.

In [7]:

S.eval('mu@100 > mu@400');

P(mu@100 > mu@400) = 0.0007986199467668083

The eval method further computes arithmetic combinations of

different parameters. In our example, bayesloop computes the joint

parameter distribution of mu and sigma for each time step. When

we ask for the probability that the ratio of mu and sigma is

greater than one, eval computes the ratio of the parameters from

their joint distribution:

In [8]:

S.eval('mu/sigma > 1', t=100);

P(mu/sigma > 1) = 0.12878704018028345

The parameter ratio above does not yet resemble the Sharpe ratio

\(S\), as the risk-free return is not inserted yet. The eval

method does not only support the parsing of parameter names, but also

the parsing of plain numbers. Below, we first check the risk-free return

at t=100, and then insert this number into the query of the eval

method. We discover that at t=100, the probability that the Sharpe

ratio \(S\) exceeds the value of one is only about 2.3%:

In [9]:

mu0[100]

Out[9]:

0.017995991983967938

In [10]:

S.eval('(mu - 0.018)/sigma > 1', t=100);

P((mu - 0.018)/sigma > 1) = 0.023246959985844733

Of course, we can also insert the risk-free return value directly, via string manipulation:

In [11]:

S.eval('(mu - ' + str(mu0[100]) + ')/sigma > 1', t=100);

P((mu - 0.017995991984)/sigma > 1) = 0.023246959985844733

The eval method contains a bit of computational overhead, as it has

to pre-process all parameter values before every single query. As we

want to compute \(p(S > 1)\) for all 500 time steps, we are better

off by using a Parser instance. The Parser is initialized only

once, and then queried repeatedly without computational overhead. Below

we show one example with a single query to the Parser instance, and

subsequently repeat the query for all time steps:

In [12]:

P = bl.Parser(S)

P('(mu - ' + str(mu0[100]) + ')/sigma > 1', t=100);

P((mu - 0.017995991984)/sigma > 1) = 0.023246959985844733

In [13]:

p_invest = []

for t in range(500):

p_invest.append(P('(mu - ' + str(mu0[t]) + ')/sigma > 1', t=t, silent=True))

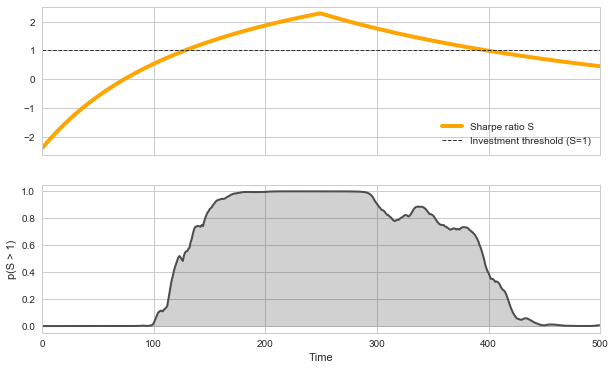

Finally, we may plot the probability that our probabilistic, time-varying Sharpe ratio \(S\) is greater than one for each time step, together with the underlying true values of \(S\) in the simulation. We find that \(p(S > 1)\) attains a value of \(\approx 0.5\) at the times when \(S=1\) in the simulation, and increases further as \(S > 1\). Consequently, we find that \(p(S > 1) < 0.5\) for \(S < 1\) in the simulation. This example thereby illustrates how the combination of inferred time-varying parameters can help to create robust indicators for desicion making in the presence of uncertainty.

In [14]:

plt.figure(figsize=(10, 6))

plt.subplot2grid((2, 1), (0, 0))

plt.plot(sharpe_sim, lw=4, c='orange', label='Sharpe ratio S')

plt.xticks([100, 200, 300, 400], ['', '', '', ''])

plt.axhline(y=1, c='0.2', ls='dashed', lw=1, label='Investment threshold (S=1)')

plt.xlim([0, 500])

plt.legend(loc='lower right')

plt.subplot2grid((2, 1), (1, 0))

plt.plot(p_invest, c='0.3', lw=2)

plt.fill_between(range(500), p_invest, 0, color='k', alpha=0.2)

plt.xlim([0, 500])

plt.ylim([-0.05, 1.05])

plt.xlabel('Time')

plt.ylabel('p(S > 1)');

So far, we have parsed either parameter names or plain numbers in the

queries to the eval method or the Parser instance. In many

applications, however, one also needs to compute the sqrt, or the

cos of a parameter. bayesloop’s probability parser therefore

allows to parse any function contained in the numpy module. Note,

however, that only functions which preserve the shape of an input array

will return valid results (e.g. using sum will not work).

In [15]:

P('sin(mu) + cos(sigma) > 1', t=50);

P(sin(mu) + cos(sigma) > 1) = 0.2479001934193268

On a final note, the Parser class also handles (hyper-)parameters of

different study instances. For example, one could imagine to run one

study S1 (which may be a Study, HyperStudy,

ChangepointStudy or an OnlineStudy) to analyze price

fluctuations of a financial asset, and another study S2 to analyze

the frequency of market-related Twitter messages. After fitting data

points, one can initialize a Parser instance that takes into account

both studies:

P = bl.Parser(S1, S2)

Note that the two studies S1 and S2 must not contain duplicate

(hyper-)parameter names! This allows to create performance indicators

that take into account different kinds of information (e.g. pricing data

and social media activity).